The American beer landscape has shifted dramatically over the past two years. What was once a stable hierarchy of familiar names has given way to new champions and surprising winners. Whether you are a casual drinker curious about what everyone else is pouring or an industry observer tracking market movements, understanding the current rankings reveals much about where American palates are headed in 2026. The story of beer in America has never been more dynamic, with established brands fighting to maintain share while newer contenders disrupt decades-old preferences.

Recent data from Circana, YouGov, and major news outlets paint a clear picture. Michelob Ultra has claimed the volume sales crown, while Modelo Especial dominates in dollar sales. Behind these headline numbers lies a fascinating story of changing consumer preferences, regional loyalties, and the ongoing battle between light beers and their full-calorie counterparts. This guide breaks down exactly which beers Americans are reaching for most often and why, drawing from multiple data sources to give you the most complete view of the current market.

Understanding Beer Rankings: Volume vs Dollar Sales

Before diving into the rankings, it helps to understand how beer popularity gets measured. Two primary metrics drive the conversation in 2026: volume sales and dollar sales. These numbers do not always tell the same story, which explains why you might see conflicting headlines about which beer reigns supreme. Understanding the difference helps explain why your grocery store might stock different leaders than your favorite bar.

Volume sales simply measure how many units gets sold, regardless of price. A 12-pack of Michelob Ultra at $18 and a 12-pack of Bud Light at $14 both count as one unit. Dollar sales, naturally, tracks the total revenue generated. This distinction matters enormously because premium beers like Modelo Especial sell fewer units but at higher price points, often outselling cheaper competitors in total revenue. A brand might sell 100 million units at $10 each while another sells 120 million units at $8 each. The first brand wins dollars while the second wins volume.

According to Bump Williams, a leading beer industry consultant, the gap between these metrics reveals important consumer behavior patterns. “When a brand leads in volume but not dollars, it tells us price-sensitive shoppers are driving that choice,” he noted in a recent USA Today interview. “When dollar sales lead volume, we see premium positioning at work.” This framework helps explain why different beers dominate different lists you might encounter online. Major news outlets often cite one metric or the other without clarifying the distinction, which leads to consumer confusion about what actually reigns supreme.

The beer industry also tracks market share, which represents a brand percentage of total category sales. A brand growing from 8% to 10% market share gains significant competitive ground, regardless of whether that reflects volume or dollar leadership. Market share data helps industry watchers understand competitive dynamics even when overall category sales fluctuate due to seasonal factors, economic conditions, or changing consumption patterns. Circana provides the primary retail tracking data that most industry analysis relies upon.

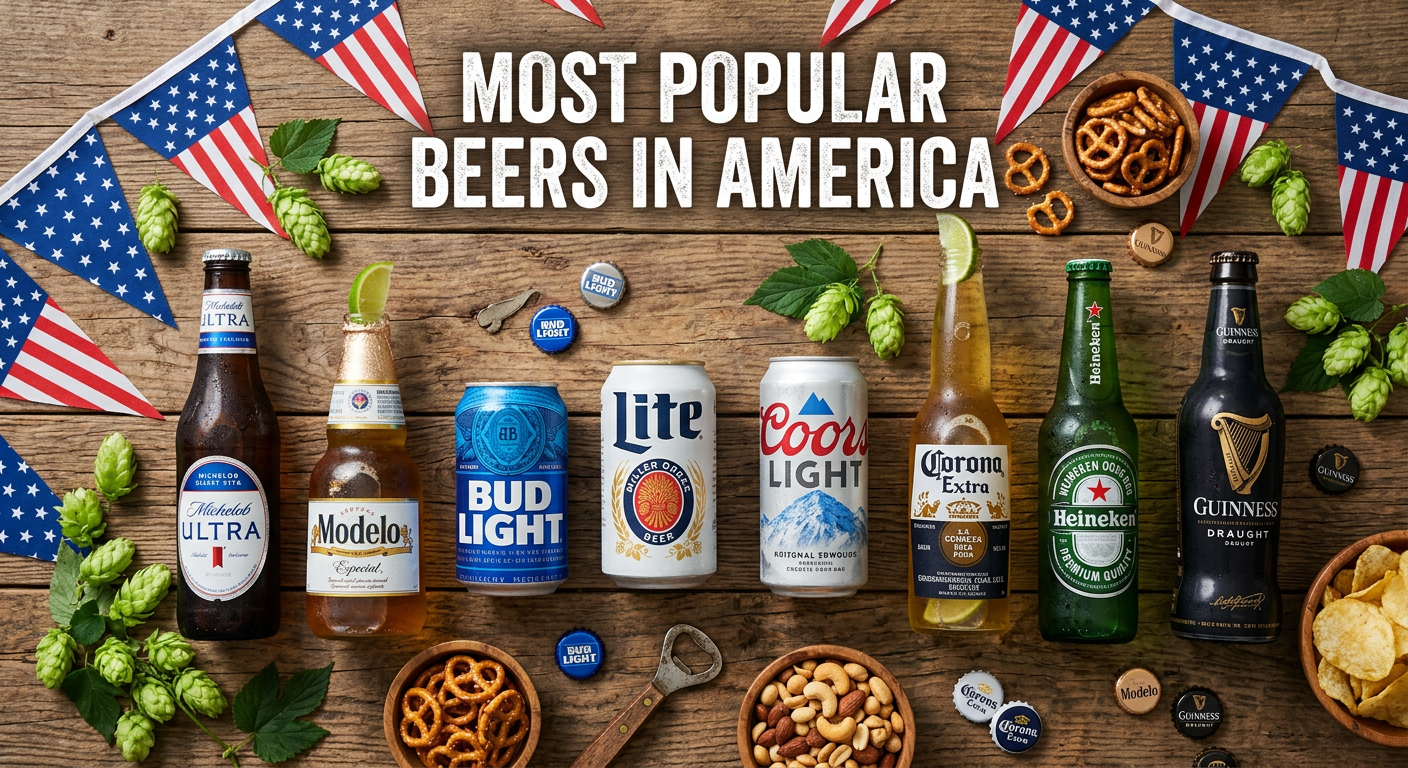

Top 10 Most Popular Beers in America Right Now (April 2026)

The data below reflects aggregated findings from Circana retail tracking, YouGov consumer surveys, and major news reporting through early 2026. These rankings represent a holistic view combining what Americans say they drink and what they actually purchase at stores and bars. We weighted consumer perception equally with actual sales data to capture both the objective market leaders and the brands people feel positive about.

1. Michelob Ultra

Michelob Ultra has ascended to the throne of American beer, claiming the #1 position by volume sales nationwide. This Anheuser-Busch product targets health-conscious consumers with just 95 calories and 2.6 grams of carbohydrates. Its marketing as a beer for active lifestyles has resonated strongly with millennials and Gen Xers who want to enjoy a drink without abandoning their fitness goals. The brand experienced explosive growth following the Bud Light boycott that began in late 2023, picking up disaffected customers who wanted a light beer that felt like a more modern choice.

What makes Michelob Ultra particularly interesting is its crossover appeal. The brand attracted consumers who might not have considered Anheuser-Busch products before, positioning itself as a premium lifestyle choice rather than simply a diet beer. This differentiation from older light beer options allowed Michelob Ultra to grow while its parent company struggled with other brands. The beer’s success demonstrates how positioning and timing can overcome even significant public relations challenges facing corporate siblings.

2. Modelo Especial

Modelo Especial holds the #1 position in dollar sales and frequently trades the overall volume crown with Michelob Ultra depending on the reporting period. Imported from Mexico and distributed by Constellation Brands, Modelo has built its reputation on a crisp, clean taste that performs well at barbecues, sporting events, and casual gatherings. The brand commands premium pricing that generates strong revenue per unit. Hispanic consumers have driven much of Modelo early adoption, though the brand has broad appeal across demographics now.

Constellation Brands has invested heavily in Modelo marketing, including NFL sponsorships and celebrity partnerships that position the beer as a mainstream choice rather than a niche import. This strategy has paid off as Modelo shed its image as a specialty beer and became a grocery store regular. The brand’s ability to maintain premium pricing while achieving volume growth demonstrates sophisticated market positioning that competitors struggle to replicate. Modelo shows how imports can achieve domestic beer scale when distribution and marketing align properly.

3. Bud Light

Bud Light remains one of America’s most recognizable beers despite losing significant market share following a 2023 advertising controversy. The brand has launched multiple marketing campaigns to win back customers, including NFL sponsorships and celebrity partnerships. Volume has stabilized but not recovered to previous levels. Still, Bud Light distribution network and brand awareness ensure it remains in the top three nationally. Industry watchers treat its recovery trajectory as a key indicator of Anheuser-Busch overall health.

The Bud Light situation offers a case study in how quickly brand equity can erode when consumers feel betrayed by corporate decisions. Even with extensive marketing investment and celebrity backing, the brand has struggled to regain its previous position. This dynamic has created opportunities for competitors like Michelob Ultra and Miller Lite, which positioned themselves as alternatives that did not carry the same perceived values. The Bud Light story demonstrates that consumer loyalty, once damaged, requires sustained effort over years rather than months to rebuild.

4. Miller Lite

Miller Lite positions itself as the original easy-drinking light beer, a distinction that resonates with long-time fans who remember when the brand launched in 1975. Molson Coors has invested in modernizing Miller Lite image while maintaining its value proposition. The beer shows particular strength in the Midwest and Mountain West regions, where Miller Time remains a cultural touchstone. Reddit discussions in beer communities frequently cite Miller Lite as a reliable, affordable choice that delivers on its promise of full flavor in a lighter package.

What sets Miller Lite apart from competitors is its positioning as the working-class choice that does not compromise on taste. While newer light beers emphasize fitness and lifestyle, Miller Lite appeals to consumers who want a straightforward, honest beer at a reasonable price. This positioning has created fierce brand loyalty that transcends occasional marketing missteps. Molson Coors has smartly avoided trying to reposition Miller Lite as premium, instead leaning into its accessible roots and value heritage.

5. Coors Light

Coors Light, Miller Lite sibling under Molson Coors, emphasizes its mountain heritage and cold-serving capability through its “cold activated” bottle technology. The brand performs especially well in Western states and has strong penetration in convenience stores where chilled availability matters. Like Miller Lite, Coors Light benefits from demographic loyalty among older consumers who grew up with the brand. Molson Coors has worked to attract younger drinkers without alienating the core customer base.

The “cold activated” marketing tagline represents one of the more distinctive product differentiators in the light beer category. The temperature-sensitive label that reveals mountains when chilled creates a functional communication of freshness that consumers respond to intuitively. This type of packaging innovation demonstrates how physical product design can support marketing claims in ways that purely advertising-based differentiation cannot achieve. Coors Light has maintained relevance through these small but meaningful product enhancements.

6. Corona Extra

Corona Extra maintains strong national presence as a Mexico-imported beer that evokes beach vibes and relaxation. Constellation Brands distributes Corona alongside Modelo, and the two brands serve somewhat different occasions. Corona leans heavily into lime-addition rituals that create distinct consumption experiences. The brand faced headwinds from anti-immigration sentiment affecting Mexican brands, but its customer loyalty remains substantial. Corona performs particularly well in Texas and Southwestern states.

The Corona lime ritual represents one of the most distinctive consumption traditions in American beer culture. Adding a lime wedge to a Corona became a social signal of relaxation and beach-side enjoyment that transcended the beer itself. This cultural embedding demonstrates how brand building extends beyond product quality into ritual creation. Even consumers who might prefer other Mexican imports often choose Corona specifically for the ritual experience it enables. Corona success story illustrates how lifestyle association can create competitive advantages that taste tests alone cannot explain.

7. Heineken

Heineken, the Dutch import, consistently ranks among America’s most popular beers regardless of which metric you examine. The green bottle has become synonymous with imported lager quality, and Heineken marketing emphasizes European heritage and premium positioning. YouGov surveys show Heineken frequently scores near the top in consumer recognition and favorability. The brand expanded domestic production to meet American demand, making it more accessible than ever while maintaining its characteristic taste.

Heineken successful navigation of the import versus domestic production question offers lessons for other premium-positioned brands. When the company began brewing Heineken in the United States, skeptics worried that American production would dilute the brand premium perception. Instead, Heineken maintained quality consistency and used domestic production to reduce costs and improve availability. This approach allowed the brand to grow volume without sacrificing the premium image that justified higher price points in the first place.

8. Budweiser

Budweiser, the original King of Beers, has experienced declining relevance as health-conscious consumers shift toward light beer options. However, Budweiser maintains fierce loyalty among certain demographics and occasions, particularly in the South and in traditional blue-collar settings. Anheuser-Busch positions Budweiser as a premium domestic option compared to its light beer siblings. The brand iconic Clydesdale imagery and Super Bowl advertising maintain cultural relevance even as volume trends downward.

The Clydesdale horses represent one of the most enduring brand assets in American advertising history. Budweiser first introduced the Clydesdales in 1933 to celebrate the end of Prohibition, and the imagery has returned periodically ever since. This heritage gives Budweiser a quality perception that newer light beers cannot match, despite whatever advantages those competitors offer in calories or carbohydrate content. The brand has successfully maintained this heritage positioning even as overall volume declines, targeting consumers who view Budweiser as an authentic American choice rather than simply another light beer alternative.

9. Guinness

Guinness represents the stout category strongest performer in American markets, demonstrating remarkable regional concentration in areas with Irish-American communities. Reddit users from South Carolina, Georgia, and New Jersey frequently cite Guinness as a local favorite that transcends typical stout positioning. The brand has expanded beyond traditional pub settings into retail channels, where its nitrogen widget cans deliver pub-quality pour at home. Guinness Draught in particular has won converts who appreciate its smooth, creamy mouthfeel.

The nitrogen widget technology that Guinness pioneered for canned beer represents a significant engineering achievement that transformed how consumers think about packaged beer quality. By replicating the nitrogen surge that occurs when a pub tap pulls a proper pour, Guinness enabled at-home consumers to experience the creamy head and smooth finish previously available only in bars. This innovation directly addressed the main complaint about canned beer versus draft, creating a competitive advantage that has sustained Guinness popularity for decades.

10. Stella Artois

Stella Artois rounds out the top ten as the Belgian import that positioned itself as a premium European lager. The brand leveraged chic advertising and restaurant partnerships to build a perception of sophistication. Stella performs well in urban markets and among consumers who view beer as part of a curated dining experience. The brand has faced pressure from competing premium imports but maintains strong distribution and recognition. Its association with the iconic chalice glass creates memorable brand imagery.

The Stella Artois chalice represents another example of how brands create distinctive consumption rituals that transcend product quality. The glass itself signals special occasions and elevated experiences, encouraging consumers to associate Stella Artois with moments worth celebrating. This positioning allows the brand to maintain premium pricing despite competition from numerous other imports offering similar taste profiles. The chalice ritual demonstrates how sensory experiences and physical objects can create brand differentiation that advertising alone cannot achieve.

Regional Beer Preferences by State

National rankings hide significant regional variation. State-by-state analysis reveals that beer preferences often follow cultural, demographic, and historical patterns that local residents recognize intuitively. Understanding these regional differences explains why your experience of American beer might differ dramatically depending on where you live or visit. These patterns reflect immigration history, local industry, climate, and cultural identity in ways that pure sales data cannot capture.

Miller brands dominate searches and sales in approximately 30 states, according to a recent Coffeeness analysis of Google Trends data. This Miller stronghold spans the upper Midwest, Great Plains, and parts of the South. The “Miller Time” branding has embedded itself into regional identity in ways that resist competition from newer entrants. When a cultural phrase becomes that deeply tied to a brand, switching costs are psychological as much as financial. Visitors to these regions quickly notice how deeply Miller Time has permeated local vocabulary and social expectations.

Guinness shows surprising strength in specific states with Irish-American heritage, particularly South Carolina, Georgia, and New Jersey. Reddit discussions in regional beer communities confirm Guinness popularity in these areas goes beyond typical stout consumption patterns. Some users report that Guinness on draft represents a bar quality indicator in these regions. The beer performance in these markets demonstrates how immigrant heritage communities shape regional tastes long after initial settlement patterns. These regional preferences often persist even as younger generations become more cosmopolitan in their tastes.

Texas presents its own distinctive preferences, with Corona, Bud Light, and local favorite Saint Arnold rounding out top choices. The Texas market size and distinct identity create opportunities for brands that invest in regional marketing. Saint Arnold, a Houston-based brewery, demonstrates how craft breweries can achieve dominant local positions when they connect with regional pride. Visitors to Texas quickly learn that local recommendations matter more than national rankings for finding authentic experiences. The Texas beer landscape shows how regional identity can support local producers even against national brands with far greater marketing budgets.

New England shows greater craft beer variety compared to other regions, with consumers demonstrating willingness to explore beyond mainstream light lagers. This regional preference aligns with the area concentration of craft breweries, higher education levels, and urban populations that value local production. Brands like Samuel Adams maintain regional strongholds here, while imports from craft-focused European countries find receptive audiences. New England consumers tend to view beer as part of food and lifestyle experiences rather than simply refreshment, creating opportunities for specialty producers that other regions do not offer.

The Pacific Northwest also demonstrates distinct preferences, with craft IPAs dominating bar menus and retail shelves. Washington and Oregon have established reputations for hop-forward beers that have influenced national craft beer trends. Even mainstream light beers face stiffer competition in these markets, where consumers demonstrate higher willingness to pay premium prices for local craft options. This regional pattern reflects both the presence of major hop producers and the cultural value that Pacific Northwest residents place on locally sourced, artisanal products.

Beer Market Trends Shaping 2026

Beyond current rankings, several structural trends are reshaping how Americans think about and consume beer. These patterns will influence rankings for years to come as the industry adapts to changing consumer expectations. Understanding these trends helps explain why specific brands are rising or falling, and where the market might head next. Industry professionals and curious consumers alike benefit from tracking these fundamental shifts in American drinking culture.

The most significant recent shift involves the rise of low-calorie, light beer options. Michelob Ultra success has validated the health-conscious positioning that once seemed counterintuitive for alcohol marketing. Consumers increasingly want to enjoy beer without the calorie consequences, and brands that deliver on this promise see growth while traditional options struggle. This trend shows no signs of reversing as New Year’s resolution culture and fitness mainstreaming influence drinking behaviors year-round. Even occasional drinkers increasingly reach for lower-calorie options that fit active lifestyles.

Non-alcoholic beer options have grown approximately 23% as more Americans explore moderation without elimination. Our comprehensive guide to non-alcoholic beer options explores this expanding category in detail. Major breweries have invested heavily in non-alcoholic versions of flagship products, recognizing that designated drivers and health-conscious moderators represent underserved market segments. The quality gap between alcoholic and non-alcoholic beer has narrowed dramatically, removing the primary barrier to adoption. Tech workers and fitness enthusiasts have led early adoption, with mainstream consumers following.

Mainstream light lagers now outsell full-calorie options across most metrics, confirming the dietary shift that began decades ago continues accelerating. This dynamic puts pressure on legacy brands that built identities around robust, full-flavored positioning. Anheuser-Busch and Molson Coors have responded by emphasizing their light beer portfolios while maintaining brands like Budweiser for customers who prefer traditional recipes. The tension between volume growth in light beer and margin preservation in premium offerings creates complex strategic challenges for major brewers who must manage portfolio cannibalization.

Craft beer continues growing as a share of total market, though consolidation among craft breweries has changed the competitive landscape. Regional craft breweries that survived the 2010s consolidation have achieved stable positions, while newer entrants face higher barriers to shelf space. Consumers have responded by becoming more sophisticated about craft provenance, asking questions about brewery ownership and production methods that would have seemed irrelevant a decade ago. This transparency demand has benefited independent craft breweries while creating challenges for brands acquired by major conglomerates.

Generation-Based Beer Preferences

Beer preferences vary significantly by generation, reflecting different formative experiences, health attitudes, and brand relationships. These demographic patterns help explain why certain brands struggle with younger consumers while maintaining strong loyalty among older drinkers. Generational analysis reveals how tastes formed in youth influence purchasing decisions decades later, and how brands must continually recruit new young consumers to maintain relevance.

Baby boomers generally prefer the beer brands they grew up with, showing strong loyalty to Budweiser, Miller Lite, and Coors Light. These consumers often have decades of brand relationship that younger consumers lack entirely. However, boomers are also the most likely generation to have reduced beer consumption for health reasons, creating volume challenges even among highly loyal customers. Brands targeting boomers must balance retention efforts against the demographic reality of aging and declining consumption per capita.

Generation X consumers demonstrate more experimental tendencies than boomers, showing willingness to try new brands and styles while maintaining some traditional favorites. This generation witnessed the craft beer revolution as adults rather than children, which influenced their willingness to pay premium prices for quality. Gen X also shows strong light beer adoption, having embraced Michelob Ultra and similar options earlier than older generations. Brands seeking Gen X attention must offer both quality consistency and occasional novelty to maintain interest.

Millennials have driven much of the craft beer movement and remain the primary consumers of specialty releases, seasonal varieties, and limited-edition offerings. This generation shows the strongest interest in beer stories, brewery provenance, and production methods. Millennials are also the primary consumers of non-alcoholic beer options, reflecting their health-conscious attitudes and openness to alternatives. Brands that tell compelling stories about heritage, ingredients, or social impact resonate particularly well with millennial consumers who use purchasing decisions to express values.

Frequently Asked Questions

What is the #1 selling beer in America?

Michelob Ultra currently holds the #1 position by volume sales in America, while Modelo Especial leads in dollar sales. The distinction matters because Michelob Ultra lower price point means it sells more units, but Modelo Especial generates more revenue per unit sold.

What are the top 5 beers in the USA?

The top 5 beers in America by volume are: Michelob Ultra, Modelo Especial, Bud Light, Miller Lite, and Coors Light. By dollar sales, the ranking shifts slightly to reflect premium positioning of brands like Modelo Especial and Guinness.

What beer is trending now?

Michelob Ultra is the fastest-growing beer brand right now, gaining significant market share following the Bud Light boycott. Low-calorie light beers and non-alcoholic options are also trending upward as consumers shift toward healthier drinking choices.

Why is Michelob Ultra so popular?

Michelob Ultra appeals to health-conscious consumers with its low calorie count (95 calories) while maintaining good taste. Its marketing as an active lifestyle beer resonates with fitness-focused millennials and Gen Xers. The brand gained substantial market share after competitors faced public relations challenges.

Conclusion

The most popular beers in America right now reflect a market in transition. Health-conscious choices like Michelob Ultra have overtaken traditional giants, while imports from Mexico maintain strong positions built on quality consistency and lifestyle branding. Regional preferences continue creating micro-markets where local loyalties trump national campaigns, demonstrating that American beer culture remains genuinely diverse despite consolidation among major breweries. These regional differences explain why national rankings never fully capture the beer drinking experience in any particular location.

Looking ahead, expect light beer and non-alcoholic categories to continue gaining share at the expense of full-calorie traditional options. The rise of Japanese beer brands in premium import segments signals another frontier where American palates may continue evolving. Whether you prefer mainstream accessibility or craft differentiation, the current landscape offers more variety than ever, even as national rankings suggest a simpler story. The American beer market rewards consumers who explore beyond headlines to discover local favorites and emerging trends that match their personal tastes.